The generalized version of Black’s formula is given by

This formula could be used to derive the European style option formulas for a derivative follows a lognormal distribution having the payoff

Where

Derivation of Black-Scholes formula using Black’s formula

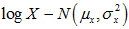

Now, we will derive Black-Scholes option pricing formula using this Black’s formula. As we know that

and

Now, we need to put these two values in Black’s formula (generalized version)

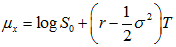

First take

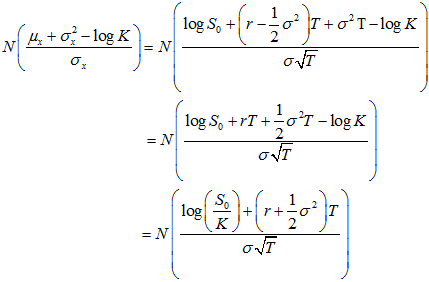

Now consider

For simplicity, we set

So, now

Hence

By putting all these values in Black’s formula, we obtain the formula for European-style call and put option formulas as follows