Square-Root Asian Option Formula Derivation

Here, we will derive formulas for European style square-root Asian call and put options when we are taking geometric average of the underlying's price.

As we know that the expectation and variance of geometric average is

Where n(a,b) represents a normal distribution with mean a and variance b. So, in case of Geometric Square-Root Asian option, we have

Where

and

Now, we need to put these two values in Black's formula (generalized version)

First take

Where

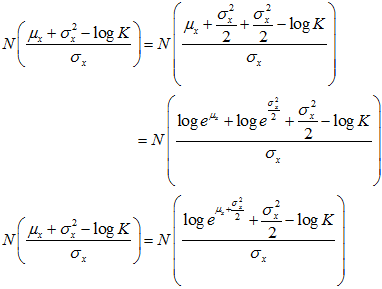

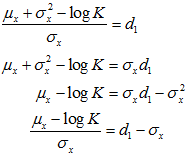

Now, consider

Using

we have

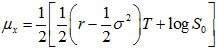

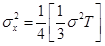

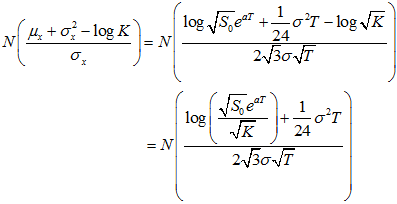

Setting

we have

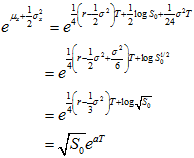

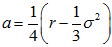

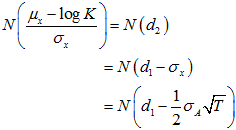

For simplicity, we set

So, now

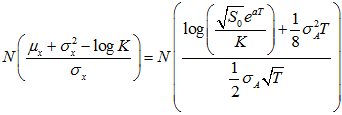

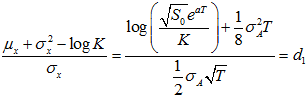

Hence,

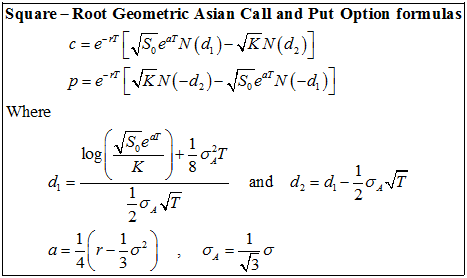

Now, by putting all values in Black's formula, we obtain the pricing formula for our geometric square-root Asian option.

|

Basic Financial terms in Corporate and Mathematical Finance |

Selection of assets, risk and return, and portfolio analysis |

View the online notes for Financial Mathematics (CT1) |

Learn Financial Computing with C++ step by step |